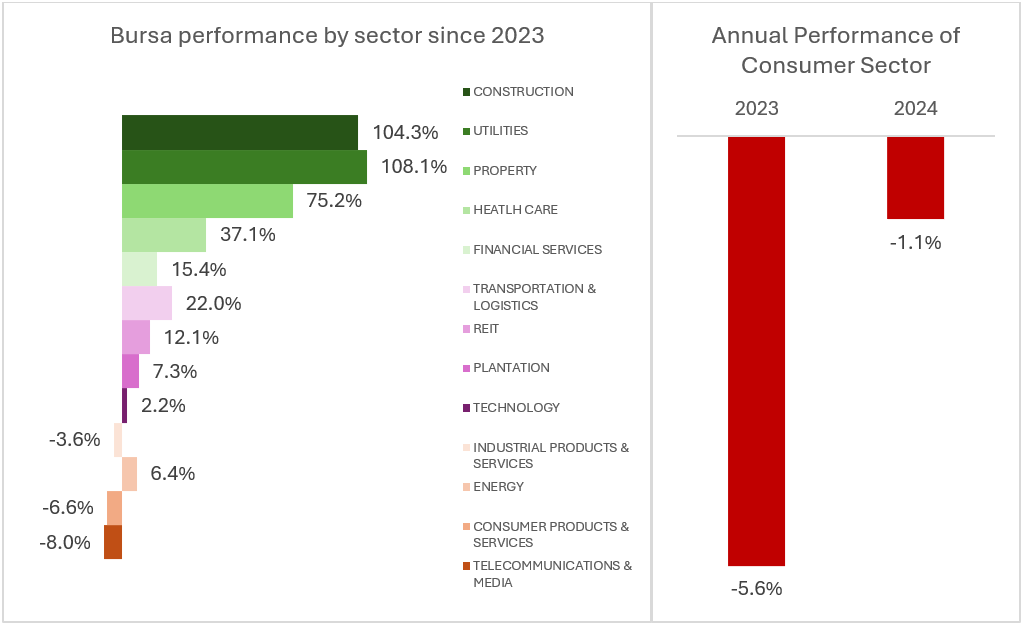

Investors in the consumer sector of Bursa Malaysia have had a period to forget in 2024 when it experienced a second consecutive year of contraction. The sector’s benchmark, the KL Consumer Product and Services Index went down by -6.6% since 2023, the worst performer only after telecommunication.

This is more frustrating if you put the performances of other sectors into context; most had gone up significantly in that same period, except for industrial, technology and those mentioned previously.

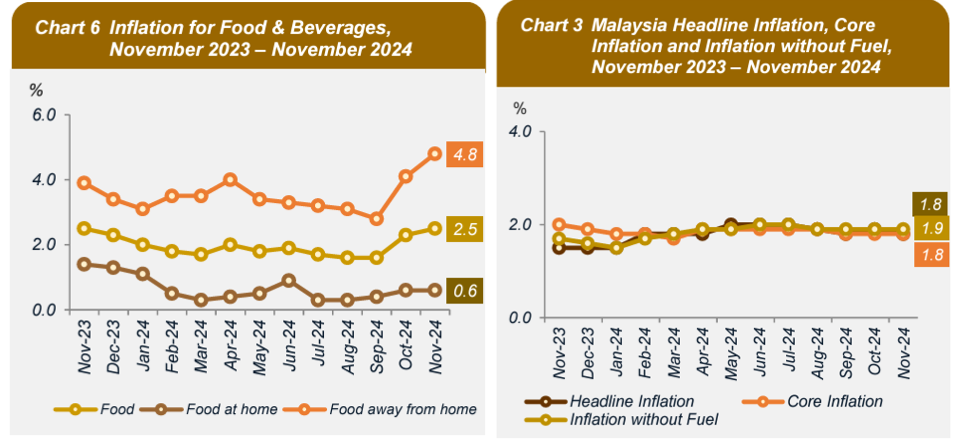

High inflation, increased business costs, lesser disposable income, and lack of catalysts were some of the reasons that were put forward to explain why.

However, this piece isn’t about dwelling in the past and crying, but seeking to understand what kind of fate may unfold for them in 2025.

I do get reminded that life moves in cycles, up down up down. Such is the nature. And this is also true for businesses and in stock markets.

“The stock market is the story of cycles and of the human behaviour that is responsible for overreactions in both directions.”

Seth Klarman,

Legendary investor and proponent of value investing

With this in mind, I’ve ventured into the sector in hope to better understand and uncover insights that may be useful for my future investing endeavours. This write-up will cover:

- What is in the consumer sector,

- Analysts market outlook,

- What does it mean to investors, and

- Top picks from analysts.

As always, this isn’t investment advice, but merely a piece for education purposes. So don’t act upon it without doing your own research.

Without further ado, let’s jump straight in.

1. What is in the consumer sector?

Businesses in this sector are those that provide goods and services directly used by individuals in their daily lives. These are items and services people buy for personal consumption, a B2C transaction and not B2B.

As of 9 Jan 2025, it’s market cap reached RM276bil, second largest only behind Financial sector at RM467bil.

Looking at the subsectors within paints a better picture of what this sector is all about. There are 8 in total. The table below shows each subsectors and their respective market cap.

| Sub Sector | Market Cap (RM mil) | Proportion of the sector |

| Food & Beverages | 86,590 | 31% |

| Retailers | 69,834 | 25% |

| Travel, Leisure & Hospitality (TLH) | 43,990 | 16% |

| Automotive | 31,181 | 11% |

| Agricultural Products | 22,353 | 8% |

| Household Goods | 10,479 | 4% |

| Personal Goods | 7,119 | 3% |

| Consumer Services | 4,361 | 2% |

| Grand Total | 275,907 | 100% |

Food and beverages, retailers, and TLH make up 72% or more than 2/3 of the overall market cap.

There are 217 companies. Big companies like NESTLE, F&N, PETDAG, 99SMART, GENTING and CAPITALA are some of the blue chips known to investors and analysts alike. Some other well-known stores and food chains in this sector include the likes of MR DIY, Family Mart (QL), Farm Fresh, Aeon, Apollo, and many others.

2. The market outlook

It’s hard to be positive when this sector has been underperforming for some time. However, historical performance does not dictate the future, and what remains in store will always be a surprise until the day it is unveiled. So without any pre-judgement, here’s what analysts have been saying about the sector:

Positive: The sector will benefit from resilient economic growth, improved labour market conditions and higher tourist arrivals expected in 2025.

Malaysia’s economy is widely expected to expand within the official forecast of 4.5%-5.5% in 2025, in line with the majority of analysts’ forecasts. Consumer spending will be the growth engine of the expansion, facilitated by stable and improved labour market. As at Oct 2024, labour force participation is hovering at a high level of 70.5%. Furthermore, private investments will add momentum to the growth.

Last year’s announcement on public and private wage rises will further improve the purchasing power of consumers. Close to RM10 bil pay hike is expected to be enjoyed by civil servants effective Dec 2024 and the new private sector’s minimum wage of RM1,700 effective Feb 2025 will add on to the spending boost.

Complimenting that is the expectation on B40 segment spending pattern to follow suit with the introduction of EPF flexible account and more government cash handouts initiatives such as Sumbangan Tunai Rahmah (STR) and Sumbangan Asas Rahmah (SARA). However, the positive impact may well be limited within the low-priced non-discretionary segment familiar to B40.

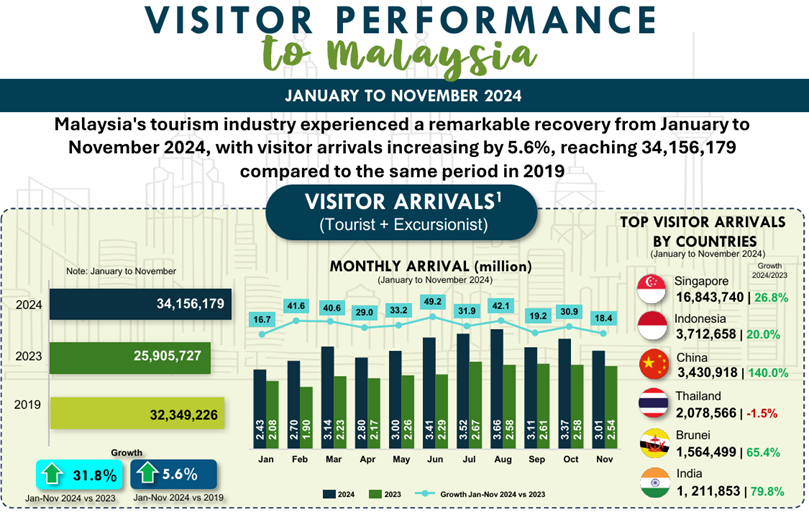

Another key driver to look forward to is the tourism activity. With Malaysia officially assuming the chair of ASEAN in 2025 and the launch of Visit Malaysia 2026, Tourism Malaysia aims to attract 35.6m international tourists, targeting tourist receipt of RM147.1bn. That is a big jump from 22.5m international tourists recorded as of the first 11 months of 2024. If the target materialises, players in TLH and F&B of the consumer sector will definitely be among the primary beneficiaries.

Negative: Rising cost of living and higher business operating expenditure (OPEX).

Despite the flowery outlook we have shared above, there are still many analysts who are quite sceptical. For starters, they viewed that spending may still be kept in check because of a potential sharper rise in the cost of living. This mainly stems from multiple factors such as:

- Electricity tariff hike – proposed mid-2025

- Subsidy rationalization (Diesel, RON95, poultry and eggs)

- Expanded sales & service tax coverage to include non-essential items, and

- Higher excise duty on sugar-sweetened beverages.

All these might potentially lead to a broad-based rise in inflation and stifle consumption despite the increase in purchasing power of consumers.

However, some analysts argue this might only impact small pockets of consumers. For example, subsidy rationalisation and new electricity tariffs will predominantly impact the heavy users of the T15 more while more muted impact will be observed among the broader population.

On the business side, there is growing concern that spending boosts of consumers may not translate to better margins for companies as the operating expenditure is expected to rise as well.

- Higher salaries from the minimum wage hike,

- Increased electricity & material costs such as fuel, and

- Increase in commodity prices that make up the raw materials.

There isn’t much room left for businesses to transfer the higher costs to consumers without impacting volume by much, especially after a series of upward price revisions seen last year on many consumer goods and services.

However there are contrary views that the margin compression would not be significant, especially given that an uptick in commodity prices for many imported raw materials can be buffered by stable ringgit in 1H 2025.

3. What does all this mean?

For businesses especially in retail and F&B, there might be a shift in building sales volumes to mitigate margin pressures. General urgency to raise product prices in order to defend margins are less likely, and companies would instead prioritise sales volume growth to grow earnings.

Many analysts that are bullish on the sector view that F&B staples would be best positioned, with consumer spending set to improve in 2025. Other retailers who are well positioned within the B40 and M40 target market with affordable and value priced items should also experience a boost in sales volume. Higher cost of living would lead consumers scaling back on discretionary spending.

Further improvements in tourism arrivals and spending after an encouraging 2024, will boost spending on familiar items such as ready-to-drink beverages and hospitality players.

4. Top picks from analysts.

From my own search, there were 3 IBs that provided their views on consumer sector in 2025. From these, I’ve compiled their outperform recommendations and the findings are as per the table below.

| Company | Kenanga | Maybank Inv | Public | Average TP | Price as at 9/1/25 | Upside |

| NESTLE | 111.65 | 111.50 | 111.58 | 95.46 | 17% | |

| MRDIY | 2.20 | 2.35 | 2.28 | 1.8 | 26% | |

| F&N | 36.30 | 36.30 | 26.96 | 35% | ||

| KAREX | 1.12 | 1.12 | 0.905 | 24% | ||

| AEON | 1.95 | 1.95 | 1.54 | 27% | ||

| DXN | 0.80 | 0.80 | 0.535 | 50% | ||

| FFB | 2.05 | 2.05 | 1.81 | 13% | ||

| LHI | 0.85 | 0.85 | 0.595 | 43% | ||

| MYNEWS | 0.80 | 0.80 | 0.67 | 19% | ||

| PADINI | 2.53 | 2.53 | 2.15 | 18% | ||

| ABLEGLOB | 2.65 | 2.65 | 1.89 | 40% | ||

| CCK | 1.75 | 1.75 | 1.53 | 14% | ||

| DKSH | 5.85 | 5.85 | 4.94 | 18% | ||

| FOCUSP | 1.00 | 1.00 | 0.81 | 23% | ||

| KAWAN | 2.45 | 2.45 | 1.63 | 50% | ||

| MAGNI | 3.02 | 3.02 | 2.49 | 21% | ||

| SPRITZER | 3.14 | 3.14 | 3.03 | 4% |

Conclusion

Like in any other sector, there are always opportunities to find stocks that are undervalued. This is more so true if you consider sectors such as the consumer goods and services that have been beaten down for some time.

As a classic Ben Graham follower, I do see an attractive pool to fish in this one – one that provides ample opportunities. However, the danger always lies in picking on value traps – stocks that are undervalued for obvious reasons; bad fundamentals.

As mentioned before, understanding the sector outlook and where it is heading helps me gauge what kind of promising stocks await for its value to be unlocked. But this is just the first step, more needs to be done especially in determining the undervaluation and margin of safety for the picks to work out.

Hence, I don’t take much consideration from analysts’ stock picks, as their recommendation may not be in tune with my investment style. But more importantly, how do I incorporate their top-down views into my calculations.

I hope you find today’s article to be useful. Drop some comments on what you think could be further considered in producing a good and reliable investment thesis.

Until then, thank you for reading and please invest safely.

Faqrul Nasrudin.